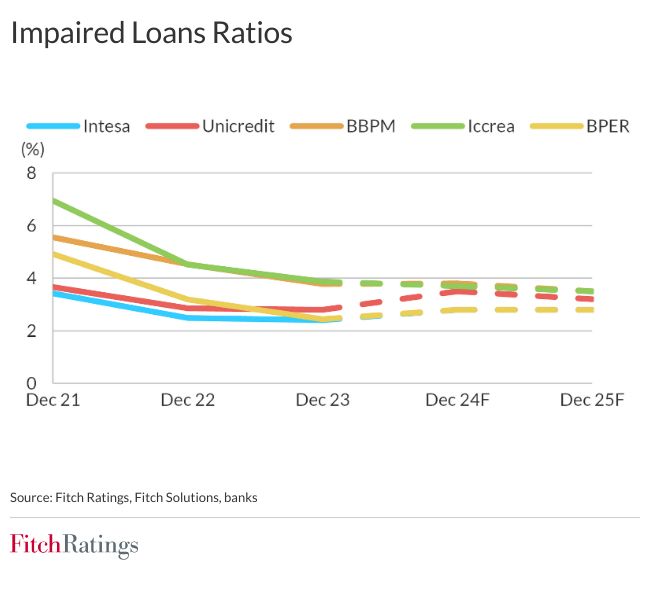

Fitch Ratings projects that impaired loan ratios at Italy’s five major banks will remain below 4% in 2024 and 2025, despite rising interest rates. Conservative lending practices, low private-sector leverage, and a slight reduction in unemployment contribute to this outlook.

In 2023, Intesa, UniCredit, Banco BPM, Iccrea, and BPER recorded their lowest impaired loan ratios in over a decade, with a median ratio of 2.8%, down from 3.2% in 2022. This is close to the European average of 2.5%. Fitch expects higher interest rates and inflation to increase these ratios, but the deterioration will be limited.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

These banks have de-risked their loan portfolios significantly through disposals, recoveries, and write-offs while tightening underwriting standards. Their corporate lending now focuses on higher credit quality firms, and sector loan concentration is limited.

The banks’ commercial real estate (CRE) exposure, relative to their common equity Tier 1 (CET1) capital, is generally lower than many large European banks. At the end of 2023, their CRE exposure was estimated at €70 billion, about 60% of their CET1 capital.

Italy’s private-sector leverage remains low by European standards, providing borrowers with more capacity to handle debt repayment pressures. Corporate debt decreased in 2023 due to lower demand and stricter bank underwriting.

Mortgage lending was subdued, and household debt-to-disposable income ratios were lower than the European average. Fitch forecasts a slight reduction in unemployment, averaging 7% in 2024–2025, down from 9% over 2019–2023, supporting asset quality.

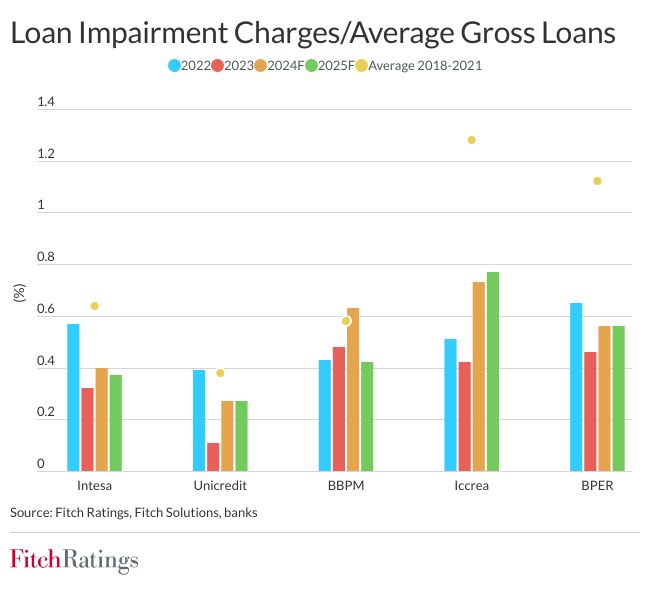

Loan impairment charges for these banks are expected to rise in 2024 but remain sustainable, between 25 and 75 basis points of gross loans annually. The banks have set aside overlays, mostly on performing loans, to cover higher provisioning needs for new impaired loans. At the end of 2023, UniCredit had overlays equivalent to 40 basis points of gross loans, BPER had 30 basis points, and the other three banks had about 20 basis points.

The median Stage 2 loan ratio was approximately 10% at the end of 2023, slightly above the European average, but with better coverage at 5%. Banco BPM’s lower coverage of 2.6% is mitigated by extensive state guarantees. These ratios reflect conservative reclassifications due to risks from the pandemic and the energy crisis. Intesa and UniCredit’s ratios also account for their exposure to Russia, which has been decreasing. Intesa’s exposure, primarily through cross-border transactions, is less than 0.1% of total assets, while UniCredit’s exposure through its Russian subsidiary is less than 0.5%.

Funding the war: the role of European banks in Russia

A return to form on the back of Cura Italia Decree