In early April, IDS announced its acquisition of White Clarke Group, a move that promises to create a secured finance IT powerhouse that will serve more than 300 banks, independents, OEM captives and speciality finance firms across North America, Europe and the Asia-Pacific. Alejandro Gonzalez caught up with IDS CEO David Hamilton to find out more.

US-based IDS is a provider of software-in-the-cloud with a reputation built on serving top-tier banks and independents who run asset finance, asset-based lending and factoring businesses and divisions within larger corporations.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

To date, IDS’s “secured finance technology” clients for its software-as-a-service (SaaS) offering are spread across North America, UK-centred Europe and the Asia-Pacific (with offices in India and Australia).

According to industry observers, IDS (International Decision Systems) is known for “offering a premium product at a premium price point”, which means mid-tier or small-tier independent or captive lessors have not traditionally been its target customer, but speaking via video conference, David Hamilton, the company’s chief executive, tells me this picture has been evolving and the recent purchase of UK-based White Clarke Group (WCG), is a clear sign of the changes afoot at the company.

Hamilton, who joined IDS as CEO in February 2018, describes the company as “a product-centric services-enabled organisation”, which under his watch has been looking “to address the large available market of small and mid-players by packaging its application to make sure its service is accessible to that market space.”

One way of achieving this market share growth is through the acquisition of similarly structured software companies that complement its geographical footprint and dovetail with its ambitions; this seems to be the IDS approach.

Soon after taking the helm at the company, IDS launched IDScloud, its “cloud software solution” in the summer of 2018, motivated by the company’s “long-term shift of enterprise computing to the cloud” and “our desire to open up markets we did not have access to in the past, due to the size and weight of our software applications,” says Hamilton.

Since Hamilton took over, IDS has been bought by Thoma Bravo, a software-focused private equity investment firm, which announced it had acquired majority ownership in IDS in October 2019 from Somers Investment Partners (SIP), formerly SV Investment Partners.

More recently, in the last 12 months, IDS has put into motion a corporate plan of building its software partnerships and setting out on an acquisitions path, Hamilton explains.

Partnerships

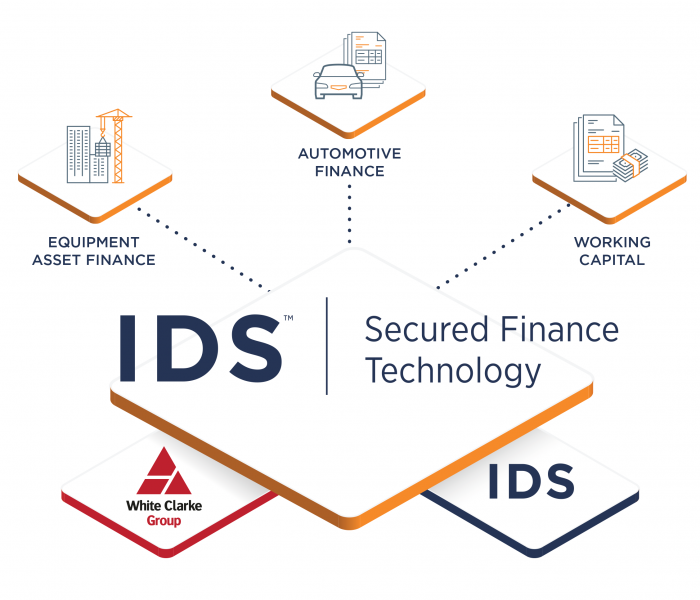

IDS’s partnerships strategy is designed to add ballast to the company’s two SaaS-enabled applications: InfoLease (its back-office lease and loan accounting platform) and Rapport (its front/middle office platform, which offers origination, credit decisions, credit underwriting, documentation and booking).

Under Hamilton, the company has migrated these software applications to the cloud and made them available to clients as a SaaS offering.

But the company has found that at the point of deploying InfoLease and Rapport, clients have come across difficulties in integrating third-party software (from invoice production and distribution to client portals) with the IDS platform. “Clients, historically, had to do this on a DIY basis because these systems were deployed on-premises,” Hamilton says.

“As part of the IDS cloud platform strategy, we want to make these solutions available through a SaaS delivery model but also curate a marketplace of pre-integrated partnerships that clients can go to in support of their business needs,” he says.

Acquisitions

Acquisitions

As far as its acquisition strategy is concerned, Hamilton says it is about “continuing to build on our US leadership with complementary products that fit with the addressable market from a growth perspective; seeking ‘geographic expansion’ in North America, Europe and the Asia-Pacific, and; exploring ‘adjacent market expansion’, essentially moving into other areas of secured finance, such as factoring and asset-based lending”.

The company’s acquisition, in February 2021, of William Stucky & Associates, a US-based provider of ABL, factoring & invoice financing software, with a European/UK footprint and 120 clients globally, ticked two of the boxes, but it is the purchase of White Clarke Group this month that “ticks all three boxes of our corporate development acquisition strategy,” says Hamilton.

“With WCG, we’ve gained a wholesale finance solution for our North American client base, both on the automotive and the captive side,” adding that geographically, the purchase “gives us tremendous scale that we don’t have in Europe and it complements our Asia-Pacific business,” supporting the strong position that both IDS and WCG enjoy in Australia.

“Also, regarding adjacent markets, we gain from technology on the automotive side to help us grow through the retail fleet and wholesale market segments,” says Hamilton.

White Clarke Group

While IDS has a significant market share in equipment and asset finance in North America (and Australia to a lesser extent), one of the attractions of the WCG acquisition, says Hamilton, is the company’s market share both in the automotive fleet and retail space in Europe. Meanwhile, WCG is a strong automotive leader in North America on the wholesale side, he adds.

“Bringing IDS and WCG together will produce a high performing, product-based, services-led organisation that will be an attractive proposition for our customers,” he says.

Hamilton, however, was not prepared to say much about the price of the deal, but he reveals that IDS’s and WCG’s yearly revenues are on par. “When WCG and IDS are brought together the size of the organisation doubles,” he says.

IDS has acquired WCG from Five Arrows Principal Investments (the European private equity arm of Rothschild & Co’s Merchant Banking), who originally invested in the business in 2016 and will remain a shareholder in the combined company.

WCG currently employs around 600 finance and technology professionals across its offices globally, according to a statement.

“WCG has more staff than we do on the services side, so we’ll be looking to capitalise on that rich talent pool of services capability they have in Europe,” says Hamilton.

The Australian-born CEO is also excited about the “impressive” metrics behind the acquisition.

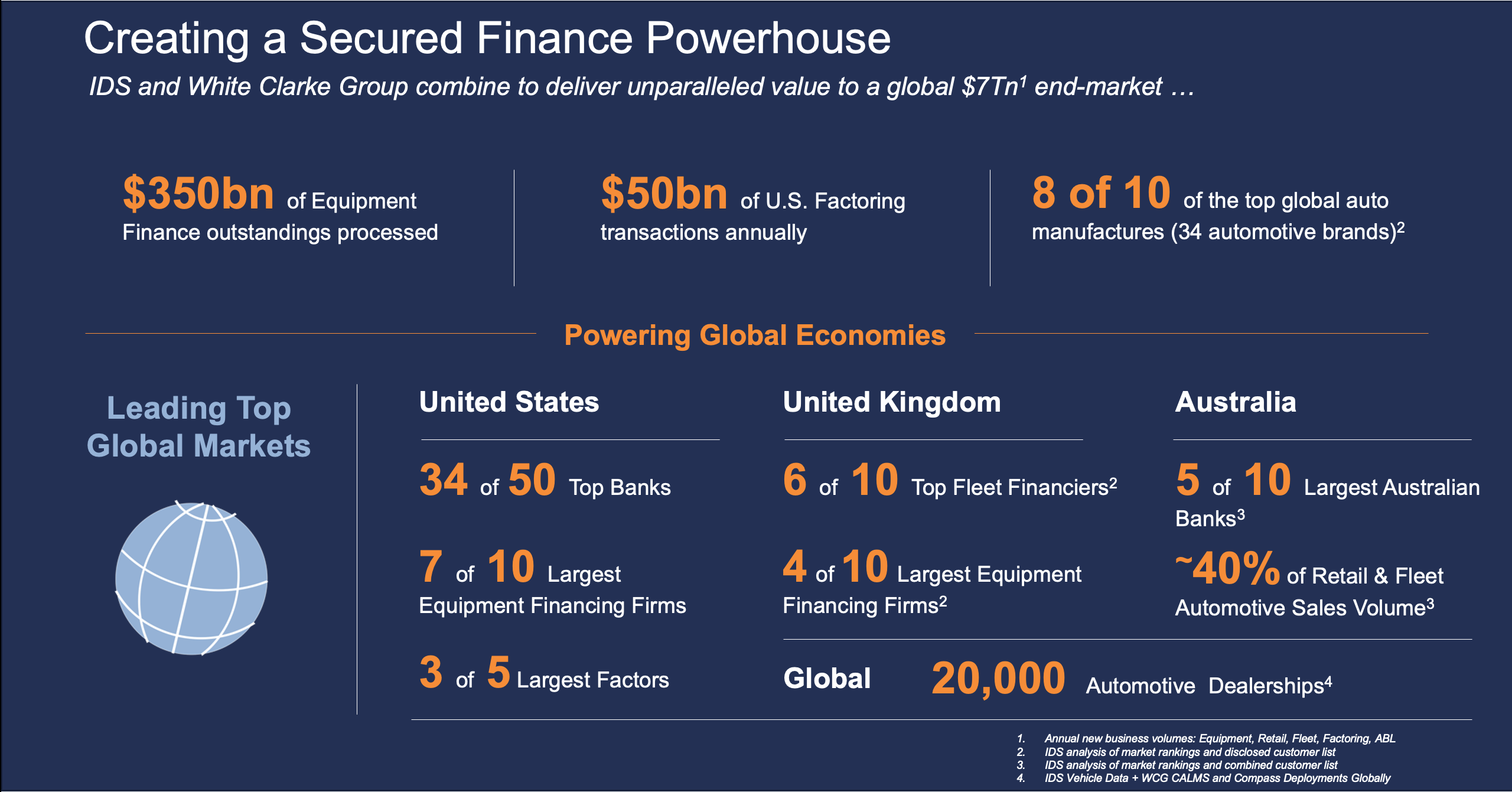

Together the companies will service more than $350bn of equipment finance in net asset values, $50bn in US factoring and eight of the top 10 global automotive manufactures, which represent 34 automotive brands in the world.

In the UK, WCG services six of the top 10 fleet financing firms and four of the top 10 large equipment finance firms, and has software deployed out through 20,000 automotive dealerships globally.

“WCG has built a strong services capability in Europe and the Asia Pacific that delivers highly tailored solutions to its client base through a strategic and configurable architecture, which is something we’re looking to capitalise on,” says Hamilton.

How likely is the company to move into general banking software? Hamilton dismisses this suggestion.

“The idea that IDS somehow becomes a provider of general banking solutions is not something we’re pursuing. Where you will see IDS continue to make investments from an acquisition, product and market positioning standpoint is around the secured finance space … unsecured finance is not for us,” Hamilton says.

Covid-19

IDS’s first cohort of early cloud platform adopters came on board in late 2018 and early 2019, with adoption growing significantly in late 2019 and through 2020.

“In 2020, we saw a slowdown in the speed at which IDScloud customers could execute the platform.

“Cloud implementation for us is usually 8-12 weeks for small-to-mid-tier lessors, we’ve moved away from long-running implementations by blueprinting and packaging solutions so it is easier and cost-effective to deploy, which, on the client-side, requires users to invest in resources and make key decision to keep the implementation on track, but with Covid, clients had to balance other factors, so we saw a slowdown in the speed at which clients could support IT projects because they needed to deploy resources elsewhere, but there was an increase in the number of adopters, we had a record year in new business sales in 2020, our top line grew in mid-double digits with IDScloud revenue growing in triple-digits year-on-year.

Currently, we have 30 clients committed to the IDScloud at close to $40bn in net asset values, says Hamilton.

Key facts: Total revenue at IDS

- 15% comes from services

- 85% comes from product licences, subscriptions and SaaS

Differences between North America & Europe

Materially there’s lots of commonality between IDS’s clients in North America and those in Europe, says David Hamilton, but there are obvious differences too.

Europe, which is characterised by “a heavy investment in in-house development and single asset-class systems” is well known for its “specialist local providers that do one particular asset class well,” whereas, in North America, “there’s not been as much in-house development of systems, generally, there’s a heavy reliance on vendor solutions (such as IDS) and a heavy focus on multi-asset class capabilities,” says Hamilton.

David Hamilton, CEO of IDS

IDS completes acquisition of White Clarke Group

IDS buys William Stucky and Associates

IDS extends cloud offering to asset-based lenders