Europe’s largest banks are in a position of strength to withstand the muted economic outlook and pockets of risks following their strong performance in the first half of 2023, Fitch Ratings says in a new report.

However, their ability to maintain good revenue in a more challenging and competitive economic environment will be crucial to absorbing higher operating and funding costs and rising loan-impairment charges (LICs) in 2H 23–2024.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

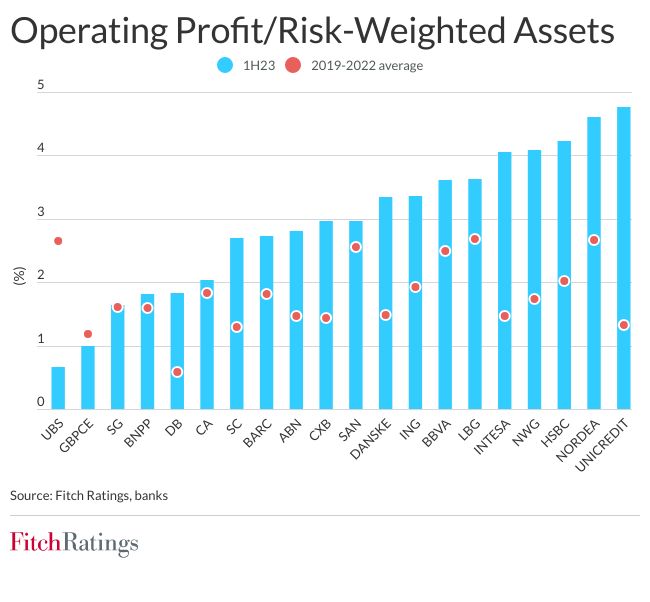

Most of the 20 large banks in Fitch’s latest quarterly credit tracker reported 1H23 operating profit/risk-weighted asset ratios well above their 2019–2022 averages as asset repricing on higher interest rates outpaced rising funding costs.

The exceptions were the French banks, whose deposit costs have increased more quickly due to the prevalence of regulated savings, and UBS, whose results were affected by the integration of Credit Suisse.

The banks will continue to benefit from high-interest rates in 2H23–2024 but net interest margins are unlikely to increase much further due to rising pass-through rates, a gradual decline in sector-wide customer deposits, peaking policy rates, slower loan growth and weaker macroeconomic prospects.

Granular deposit bases have helped to limit deposit outflows and support liquidity, and asset quality metrics have been stable as monetary tightening is taking time to affect the real economy.

The banks’ median impaired loans ratio was 2.4% at end-June 2023, with the highest ratios being 3%–4% for banks in southern Europe or with exposure to emerging markets.

Asset quality will weaken in 2H23–2024, particularly for SME lending, consumer finance, and commercial real estate portfolios.

However, we expect only a moderate rise in unemployment, which should support asset quality, and the banks’ average LIC should remain low by historical averages (1H23: 29bp of gross loans).

HSBC and Lloyds included in Which? ‘red’ warning of UK banks with poor green credentials