Global aircraft lessors’ recent 1Q 2020 financial results confirm issuers’ continued efforts to maintain sufficient liquidity amid the economic fallout from the coronavirus pandemic, according to Fitch Ratings.

The pandemic has caused significantly reduced passenger air travel, aircraft utilisation rates, lease collections and cash flows. However, lessors have sufficient headroom within current ratings, Fitch found.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Rated lessors should withstand Fitch’s base case scenario without breaching leverage or liquidity downgrade triggers, given reduced purchase commitments, manageable debt maturities over the next 12 months, and, in some cases, recent draws on available borrowing capacity, the rating agency said.

Fitch revised its global aircraft leasing sector outlook to ‘negative’ from ‘stable’ on 16 March and took negative rating actions on aircraft lessors on 23 March.

Key near-to-medium term rating sensitivities, aside from liquidity management, include the pandemic’s effect on operating cash flow given increased lease deferrals and/or defaults, the impact of potential airline bankruptcies, aircraft repossessions and higher potential leverage due to impairments.

Fitch-rated aircraft lessors reported that nearly 90% of airlines have requested rent deferrals. However, deferrals have only been granted to a select number and typically for two to three months, with payback following the deferral period, including interest.

For rated lessors, contracted rent deferrals ranged from 2% to 12% of annual rental revenues, which Fitch believes is manageable.

A second round of rent deferral requests is possible, depending on the length of lockdown measures and the pace of travel demand recovery, which would further impair aircraft lessor operating cash flow generation in the second half of 2020.

Some lessors have drawn on bank revolvers, while most have cancelled nearly 40% of near-term orders for unplaced aircraft to shore up liquidity and reduced near-term funding needs, which Fitch views as a credit positive.

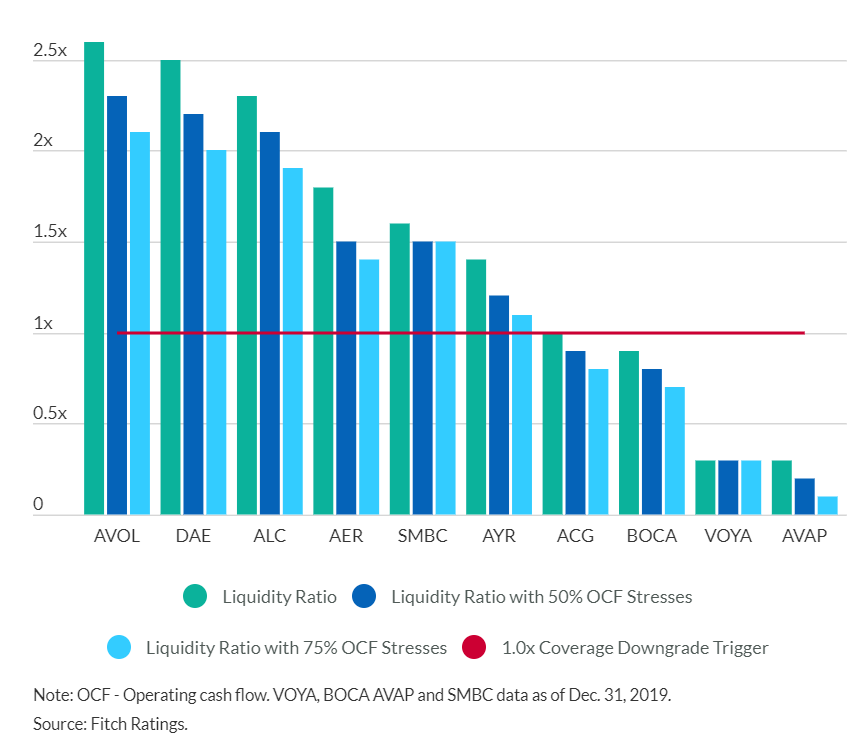

Issuers have sufficient liquidity to withstand near-term reductions in financing availability and lease cash flows amid the declines in air traffic. As of 31 March 2020, aggregate liquidity sources of rated aircraft lessors covered uses by approximately 1.6x, representing a sufficient cushion relative to Fitch’s 1.0x downgrade trigger, although continued deferrals and defaults will reduce liquidity cushions.

Only Voyager Aviation Holdings, LLC (rated ‘BB-‘/Rating Watch Negative [RWN]) and Avation plc (rated ‘B’/RWN) have reported ratios below 1.0x.

An increase in aircraft repossessions could reduce residual values, resulting in impairment charges. However, no material impairments have yet been reported by rated lessors given limited airline liquidations and related repossession/aircraft sale activity.

As of Q1 2020, most standalone investment-grade aircraft lessors had the capacity to withstand impairments of 4% of fleet net book value before exceeding Fitch’s 3.0x downgrade trigger.

The highest four-year average impairments comparatively reported in 2016-2019 was 1.6% across Fitch-rated lessors, driven by assets sales rather than aircraft value depreciation.

Fitch’s global base-case economic outlook assumes easing of the pandemic in the second half of 2020 and increased broad economic activity, as inventories are rebuilt and some consumer and capital spending is re-profiled, the company said.

Aggressive macro policy responses – emergency interest rate cuts, massive central bank liquidity injections, macro-prudential easing, credit guarantee schemes and substantive fiscal stimulus – should also start supporting growth from the second half of 2020.

However, GDP is unlikely to reach pre-virus levels before mid-2022 in the US and significantly later in Europe.

Fitch’s downside scenario assumes a lengthier and more pronounced economic decline under which some aircraft lessors with more limited financial flexibility could breach Fitch’s leverage and/or liquidity downgrade triggers resulting from elevated airline defaults and deferrals leading to higher impairments.

Issuers that have already been downgraded and/or placed on RWN have weaker liquidity positions (particularly in the event of materially reduced cash flow), limited capitalisation headroom to withstand moderate impairments, older aircraft with concentrations and/or elevated exposure to less liquid aircraft types.

Liquidity coverage holds up under stress

Aggregate liquidity sources covered 12 months of debt maturities, capital expenditures by ~1.6x as of 31 March 2020