The profitability of Europe’s largest banks will normalise later this year after lenders recorded one of the strongest sets of quarterly results in recent history in the first quarter of 2023, Fitch Ratings said in a report.

“We expect rising funding costs, higher loan impairment charges (LICs) and slower loan growth to restrain profitability in the second half of 2023,” it said.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Most of the 20 large banks in Fitch’s latest quarterly credit tracker had a strong start to 2023 “as the repricing of assets on higher interest rates outpaced the increase in funding costs and LICs remained low,” the agency said.

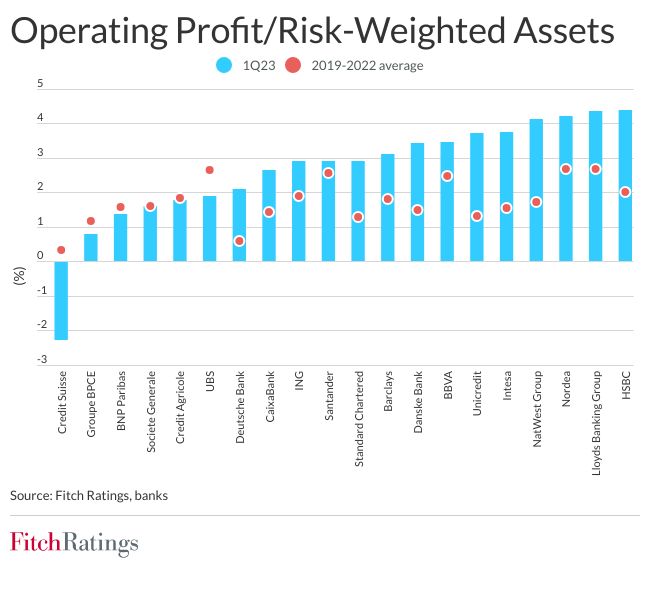

European bank results

The banks’ median annualised operating profit to risk-weighted assets in 1Q23 was 2.9%, compared with 1.9% in 1Q22.

Only Credit Suisse made an operating loss, while the four largest French banks (Credit Agricole, Societe Generale, BNP Paribas and Groupe BPCE) underperformed due to pressure on domestic net interest margins as liabilities repriced faster than assets.

With the notable exception of Credit Suisse, the banks withstood the market volatility in 1Q23, helped by granular and stable deposit bases along with strong funding franchises. Asset quality metrics remained robust, with the impact of monetary tightening yet to feed through significantly to the economy.

As 2023 progresses, higher interest rates will increasingly affect funding costs due to higher pass-through rates for deposits, switches into costlier deposits and higher wholesale funding costs. In many cases, net interest margins may be close to peaking.

LICs are likely to gradually increase in the second half of 2023 as high-interest rates and persistent inflation put pressure on borrowers. However, the impact should be limited as the banks have been building provisions in anticipation of asset-quality deterioration, the agency said.

Fitch said it expects LICs for 2023 to be in line with the banks’ guidance, typically 20bp-40bp of gross loans. In addition, low unemployment should continue to support asset quality.

How SMEs can remain buoyant and navigate the rest of a choppy 2023: Bibby Leasing