A new kind of small business lending provider will emerge from the Covid-19 experience writes Martin McCann, founder and chief executive of Trade Ledger

—-OOOO—-

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Across Europe, the Covid-19 lockdown is coming to an end. After weeks of suspended economic activity and millions of people working from home, economic activity is beginning to restart.

In parallel, we will now be able to assess what lasting change will emerge from this period.

Our guess is that, in the near term, it might look superficially like not much has changed, but the lockdown has been enough time for new habits to form and for change to be accelerated. The future has been brought forward.

In the realm of business lending, the pandemic provided a massive test to traditional lenders, most of whom failed it.

It shone a light on years of underinvestment in systems and processes that were built for a time of branch- and paper-based banking and could not cope with the spike in demand, leaving thousands of businesses without cash.

In the short term, we can expect customers who were let down in their time of need to look for new banking providers.

But, over the medium term, we can expect both new entrants into the market, as well as significant investments in new systems, now it is clear that lending infrastructure needs to upgraded to meet the demands of a digital economy.

However, what is less clear, is what that digital future will really look like. It is not about making lending services available through digital channels – or at least that is not the end state.

Instead, we are seeing something much bigger. What digitisation really means is that everything becomes connected thanks to ubiquitous computing.

What arises, as a result, is an immense stream of valuable data that allows for all services, including lending, to be delivered at higher quality at scale. It will precipitate not the end of paperwork, but the move to embedded or open finance.

What arises, as a result, is an immense stream of valuable data that allows for all services, including lending, to be delivered at higher quality at scale. It will precipitate not the end of paperwork, but the move to embedded or open finance.

Major shifts

Here are five ways we think business lending will be transformed post-pandemic

1. A shift to Virtual – not just digital

One thing this pandemic has really brought home to banks is that digitalisation cannot just apply to customers. Banks have been investing for over a decade in customer innovation, but have spent comparatively little time and money on true digital innovation in the middle and back-office.

In their new guise as virtual banks, with hundreds of thousands of support and operational staff working remotely, the underinvestment in banks’ own systems has been laid bare as critical functions competed for wifi bandwidth with kids streaming videos and as important calls were punctuated with barking dogs.

2. Embedded lending

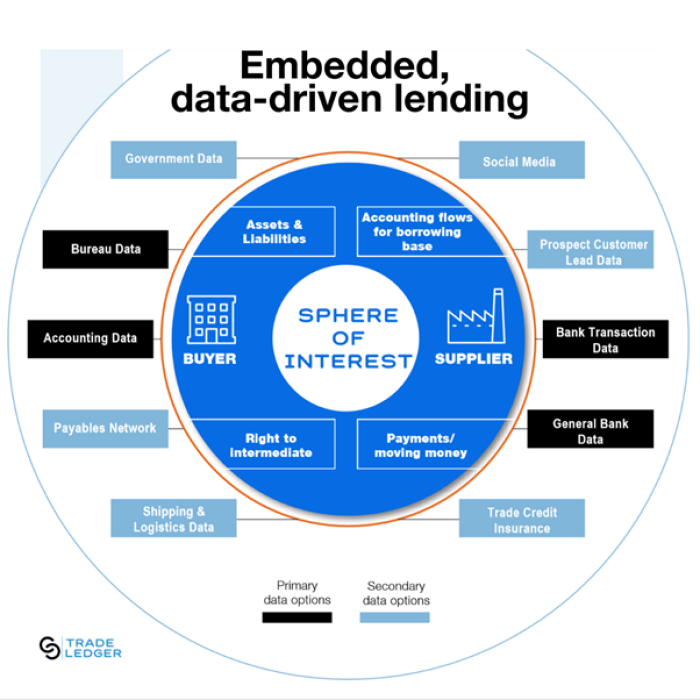

The ultimate destination for digital lending won’t be that we can apply for loans through our mobile phones. Instead, once lending has been digitized it will become akin to an infrastructure layer that can be embedded into other services.

That means that lending will be available seamlessly when we need it, such at the point of buying inventory on the Amazon Marketplace, or when we’re reconciling our monthly accounts on Xero.

3. Data-driven – fostering a new level of personalization and value-add

Not only are data sources becoming real-time, but they are proliferating and becoming easier to access through API-based, system to system connectivity. Now it is up to lenders to bring together these multiple data sets – structured and unstructured, financial and contextual, internal and external – into a unified data model that is capable of delivering a completely new level of value-add to customers.

With the right data insights, lenders will be in a position to move from standard products based on standard terms to completely flexible services based on the exact context of every customer – giving them the funding they need at the time they need it.

4. Increasing return on trust

4. Increasing return on trust

Up until now, the limits of data sharing have not been set, nor solved, by legislation. Instead, what stops the free flow of data in the information age has only been questions of trust and value-add. We predict, in the context of data-driven lending, trust will be made more explicit through consent management and returns on the information shared will be more carefully tracked.

But we also predict that trust will work both ways. Where customers share more data, lenders will better tailor lending services, insights and advice, which in turn will lead customers to share more date.

But conversely, where customers choose not to share data, they face not just less customized services, but also likely higher rates. That is, an information asymmetry will grow up between companies that share data and those that do not, where the latter will be subject to adverse selection penalized with higher rates.

So, in effect, data sharing will be compelled by both the carrot of better services and the stick of higher rates.

5. Intelligent ecosystems

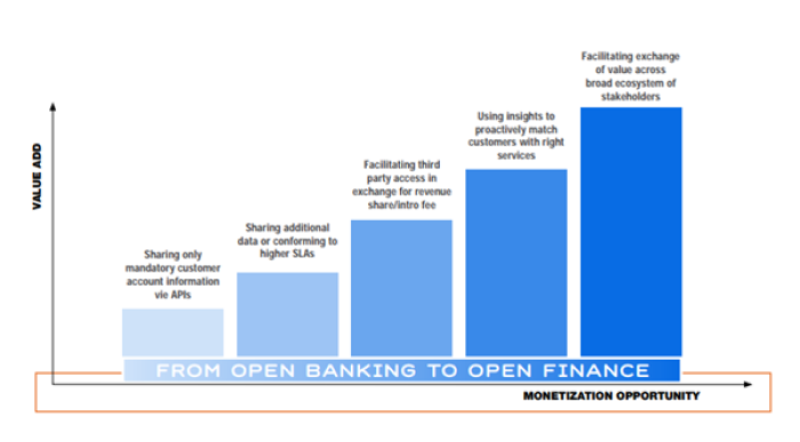

The proliferation of data will not only improve personalisation but will also facilitate new lending ecosystems; a move towards what we term open finance.

Open finance refers to the free exchange of all customer data that can be used to deliver better outcomes for that consumer. It is happening already with real-time accounting information, but it will soon extend to areas like goods in transit and inventory – after all, it all data that belongs to the customer.

Once lending has become intelligent in making individual lending decisions, the next step will be to use the information generated from Open Finance to link together the different stakeholders in the value chain – banks with fintechs, consumers with fintechs, banks with banks and so on – to create intelligent ecosystems that deliver even more value by creating optimised, meta-services.

Better quality at higher scale

Better quality at higher scale

To quote Babak Nivi, co-founder of Angel List, there is no longer a trade-off between scale, on the one hand, and quality, on the other; instead, digitization is about pursuing “quality and scale, simultaneously”.

Business lending has, until now, been ruled by this trade-off. Financial institutions took the time to make high-quality credit decisions, but this couldn’t be done at the scale needed – leading to a $1 trillion-plus funding gap for SMEs pre-pandemic and the bankruptcy of thousands of SMEs during the pandemic.

But with digitisation, the trade-off has disappeared. Lending technology can be scaled to meet the demands of SMEs – even in a crisis – at the same time as it can be used to make that lending ever more tailored to the individual context and delivered at the time of need.

Therefore, even though it might not feel like it right now as we address its fallout, the pandemic is catalyzing an upgrade to digital lending that will lead to faster growth and increased economic mobility.

This article is based on Catalyzing Positive Change: business lending in the post-pandemic era, by Martin McCann, founder and chief executive of Trade Ledger