There’s no reason why backwards-looking economic data and forecast data should look alike, clearly, they are addressing different scenarios, draw on different datasets and are based on different assumptions, but the contrast between the two became surprisingly stark in June when the OECD and the BCC issued their outlooks for 2022 and beyond.

Forward-looking data

If the Organisation for Economic Co-operation and Development is correct, once Russia is removed from its economic forecasting statistics, the UK will be the worst-performing economy among the G20 group of leading developed economies in 2022.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

In a similar vein, the Britsh Chambers of Commerce (BCC), which represents tens of thousands of businesses across the UK of all sizes, says this year will see no growth in the 2nd and 3rd quarters and a shrinking of the economy of 0.2% in the final quarter of the year.

What does this mean for businesses? Costs of all types are expected to increase, from energy prices, shipping costs and raw materials. Also, demands for improved wages are expected to rise as the cost-of-living crisis begins to bite.

As margins narrow, businesses will be faced with making tough decisions about passing costs onto customers and/or making cuts and restructuring how they operate. In some cases, winding up the business or filing for bankruptcy will be the only solution. Those who do run viable operations will likely put off new investments as they look to hold on to their cash, particularly as customers defer spending given the uncertain outlook for 2022.

Backwards-looking data

Against this gloomy backdrop, is backwards-looking data issued recently, and independently, by UK Finance and Acquis.

According to UK Finance, bank lending in the first quarter of 2022 has signalled a gradual return to normal lending to SMEs across the UK.

A recent review, by the trade association for the UK banking and financial services sector, found a pickup in demand for cashflow finance through overdrafts and invoice finance and asset-based lending. It described this as “a consequence of both the end of Covid-19 restrictions and the significant increase in cost pressures that many businesses are now facing.”

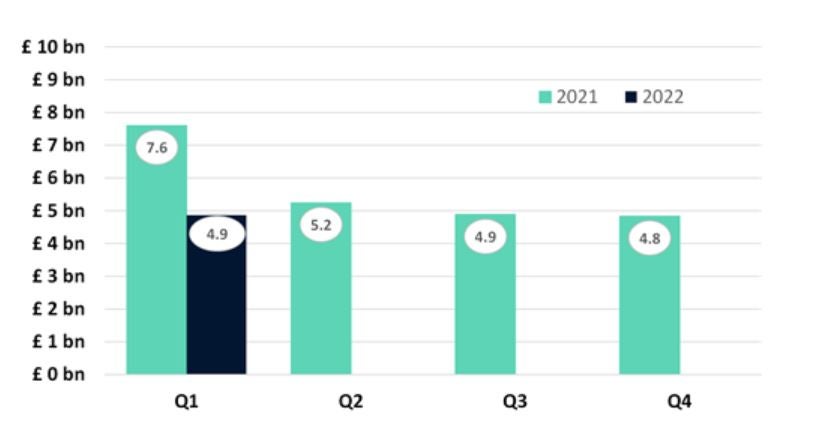

Gross lending to SMEs through loans and overdrafts

Following the significant growth in lending volumes in 2020/21 from the government’s Covid-19 lending schemes, demand for finance has been comparatively muted over the past year with gross lending of around £5bn per quarter from the high street banks covered in our sample, the trade body said.

During the first quarter of 2022 gross lending to SMEs was £4.9bn, £0.1bn higher than the previous quarter.

Stephen Pegge, managing director of commercial finance, said: “Finance usage and demand by SMEs shifted little in the early months of 2022. Overall lending has been broadly stable, but there has been a modest pick-up in new overdraft approvals and utilisation in addition to continued growth in invoice finance and asset-based lending advances. This is likely a response to the now complete reopening of all parts of the economy as well as the increase in cost pressures.”

Acquis

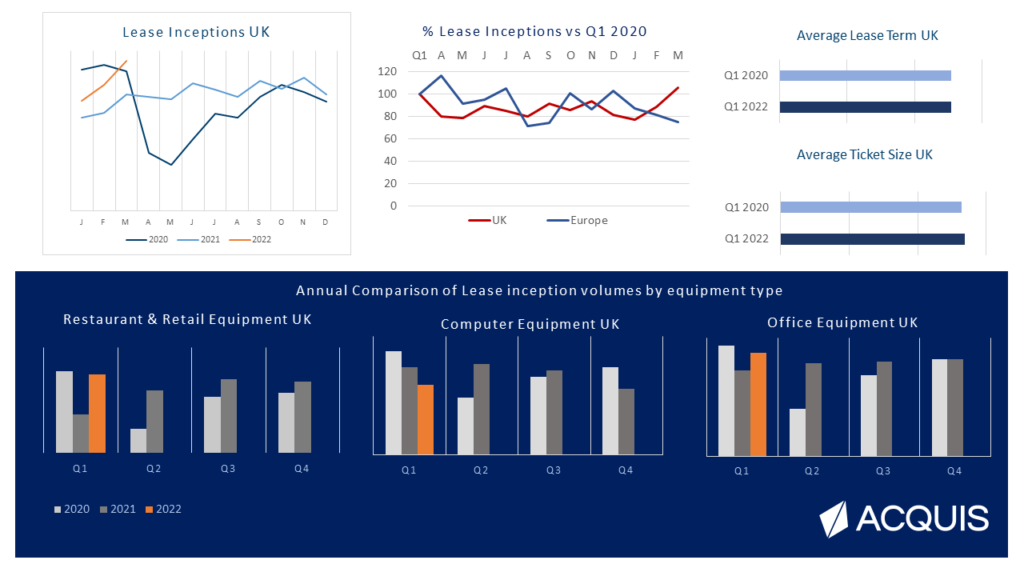

The bankers’ report chimes with the Acquis Index for Q1 2022, which has revealed that businesses (for now) are leasing more essential items at the end of the period compared with this time last year (albeit from a relatively low base).

The latest Index – an economic indicator of how much equipment UK companies lease – has found that the proportion of new contracts signed by UK companies to lease essential items: is 29% higher than in March 2021, when the UK had been battered by the pandemic and was entering the third month of its third national lockdown, and is 8% ahead of the equivalent point in 2020 when the impact of the pandemic was yet to hit fully.

“By comparing pre-pandemic performance during Q1 2020 with current performance two years later in Q1 2022 – we can see that the recovery in the UK leapt ahead of Europe with volumes for the entire quarter tracking ahead of where they were before the pandemic hit, for the first time since the pandemic began, while in Europe volumes were over 20% down on pre-pandemic performance,” Acquis said.

The adage, “past performance is not a guarantee of future results” is well known in the investment world but is equally true when comparing backwards data with forecasts, one observer of UK leasing told me.

The same observer also said it is best to consult backwards-looking data when dealing with mature markets and a stable economic environment. That seems a tall ask these days when – it could be argued – that the commercial lending market is mature but the economic environment is certainly not stable.