Paul Hollingsworth, chief European economist at BNP Paribas (UK) considers the backdrop to the monthly GDP estimates issued by the UK’s Office for National Statistics on 11 April 2022.

At face value, the ONS’s monthly GDP figures for February were disappointing. However, with underlying momentum better than the headline figures suggested, and inflation still moving higher, we do not think these figures will dissuade the Bank of England’s Monetary Policy Committee from hiking again at its May meeting.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

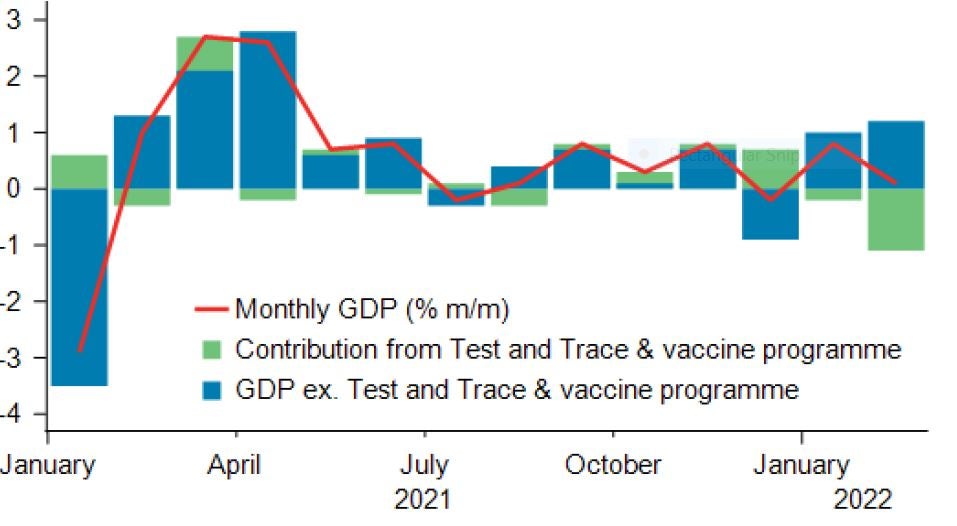

While the 0.1% month-on-month rise in GDP was lower than the consensus estimate of 0.2% and our own forecast of 0.3%, we would note that lower expenditure on the vaccination and test and trace programmes shaved a whopping 1.1 percentage points of GDP. After removing this component, GDP growth actually accelerated from 1% in January to 1.1% in February.

Contributions to month-on-month change in UK real GDP (% pts)

Similarly, consumer-facing services recorded a 0.7% month-on-month expansion in February, after growing by a robust 2% in January (which in turn was upwardly revised by 0.3 percentage points). In particular, there was a sign of a strong post-Omicron bounce-back in demand for hotels.

With consumer services still 5.2% below the pre-pandemic level, there is scope for continued catch-up reflecting an ongoing rotation in demand.

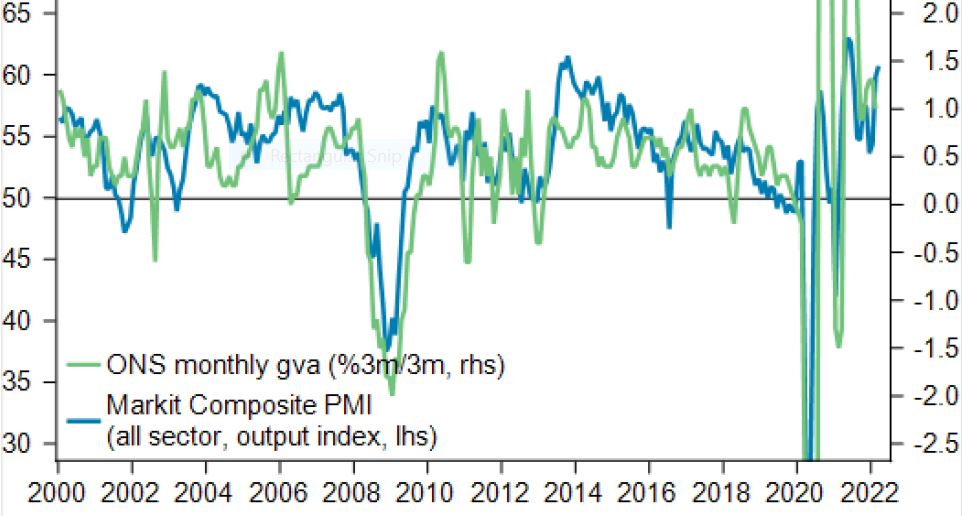

What’s more, surveys have remained relatively buoyant. For example, the composite PMI (purchasing managers’ index) actually picked up in March and is consistent on the basis of past form with a robust quarterly growth rate.

PMI vs GDP

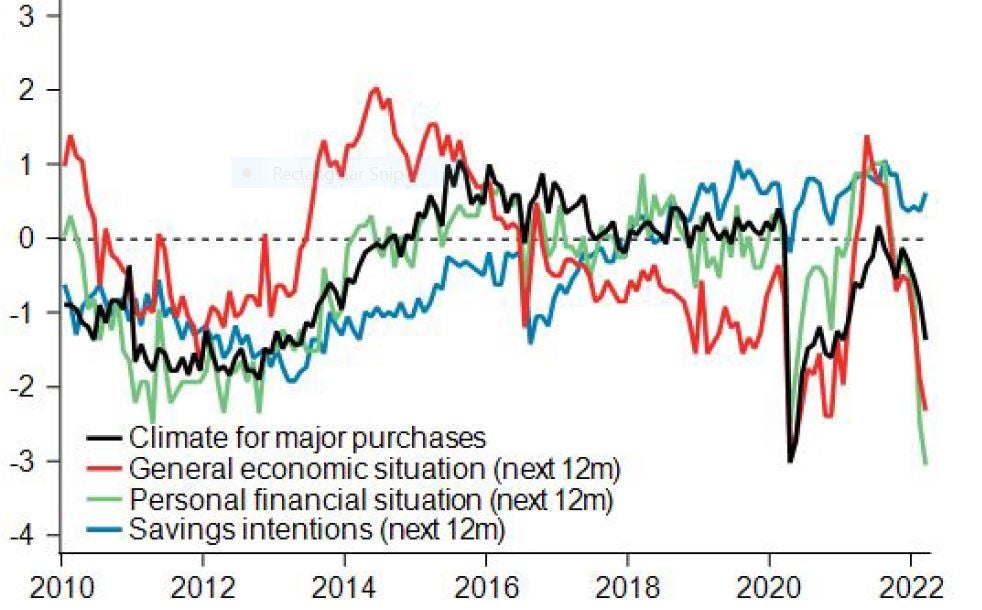

Looking ahead, however, we are less confident that this strength will persist. For starters, the squeeze on real incomes is intensifying at the same time as consumer confidence is falling, pointing to a weaker backdrop for consumption in the near term.

GfK consumer confidence indices

Second, the ONS figures paint a weak picture for industry, and in particular automotive producers. With the Russia-Ukraine conflict exacerbating supply chain issues while higher energy prices squeeze profitability, near-term prospects for the industry remain weak too.

Third, Government estimates suggest that the additional bank holiday on 3 June to celebrate the Queen’s Platinum Jubilee is likely to weigh on GDP in Q2 – even if it is partly made up for in Q3.

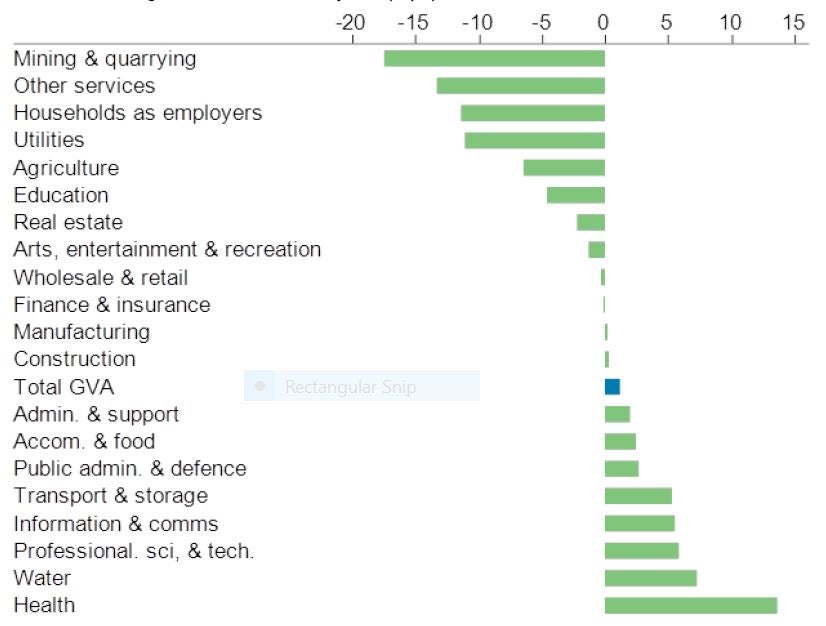

Finally, the contribution to GDP from healthcare – which has been the single largest contributor to GDP since January 2020 – is likely to fade now that Covid-related spending (e.g. on free testing) is being phased out.

Contribution to change in UK GDP since January 2020 (% pts)

On balance then, we think today’s data are unlikely to shift the dial on near-term prospects for further policy tightening from the MPC. But gathering headwinds are likely to mean a slower pace of tightening over the year as a whole than markets currently expect.