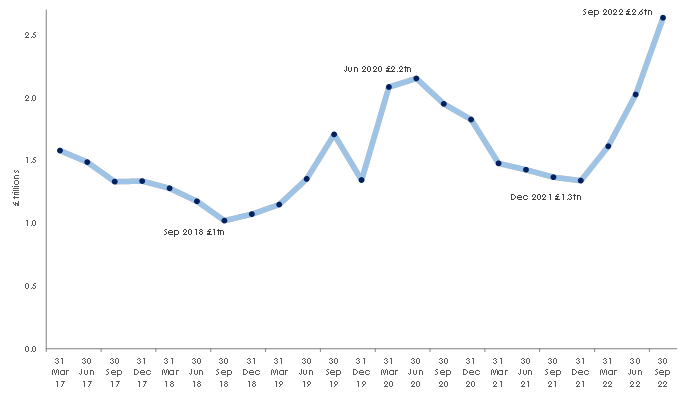

The value of interest rate swaps held by banks in the UK reached £2.6 trillion on 30 September 2022, up 93% from £1.3tn in just nine months, from 31 December 2021, as businesses rushed to protect themselves against interest rate rises, said ACP Altenburg Advisory, a debt advisory specialist. That is the highest value for interest rate swaps held by banks since 2013.

Interest rate swaps are used to help protect businesses from rising interest rates. The swaps allow businesses to fix the interest rates payable on their loans, regardless of how the Bank of England base rate moves during the term of the swap. Sales of interest swaps have soared since the Bank of England started raising rates in December 2021.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

The value of interest rate swaps rose sharply as businesses hedged floating-rate loans

However, Altenburg warns businesses that they should consider alternative options and take professional advice before locking themselves into an interest rate swap agreement. While swaps allow businesses to have certainty over their costs of borrowing during a period of rising interest rates, they can also fix those interest rates at what could prove to be too high a level.

Swap rates are based on current market expectations for future interest rate movements (plus an element of profit for the provider of the swap). However, history has shown that market expectations are typically only a somewhat accurate predictor of the near-term direction of interest rate changes. Beyond that, market expectations have not generally been accurate as they tend not to predict further away and less certain events.

Should market conditions change and the base rate fall further than expected over the next few years, businesses could find that their swaps have fixed their interest rates at above-market levels for a significant period. Under those circumstances, the swaps could also carry substantial costs if borrowers wish to exit them.

Expectations have grown in recent weeks that the Bank of England’s programme of rate rises may moderate in 2023. The market expectation of the peak Base Rate has fallen from c.5% to c.4.5%, with rates now expected to decline to 3% over the next 5 years after the peak.

Will Senbanjo, Partner at Altenburg, said that there are other products available that may be more suitable for businesses seeking to control their costs of borrowing. They include:

- Interest rate caps – these products place a limit on how high a floating interest rate can rise, but allow the business to benefit from future interest rate falls. Interest rate caps have to be bought and so are an upfront cost for a business to fund

- Interest rate collars – ensure interest rates can only move within a limited range with both a maximum rate and a minimum rate and can be structured so that they have no upfront cost to the business

Will Senbanjo said: “Banks are selling a lot of swaps at the moment – but interest rates may not rise as high as expected. Some businesses could well find a swap agreement costs them a lot more than necessary over the coming years.”

“It’s understandable that in a time of rising rates, businesses would want certainty rather than risking a large increase in interest costs with a floating-rate loan. However, if inflation moderates in 2023 and the Base Rate does not increase as much as expected, using alternatives such as caps and collars could allow businesses to benefit from the new market conditions.”

“These alternatives may give businesses a competitive advantage over to peers that have locked in at current swap rates.”

“With the UK’s interest rate picture still cloudy in the medium and long term, businesses should look carefully at alternatives to an interest rate swap agreement.”